Featured

Table of Contents

Techniques for Lowering Credit Card Interest in Surprise Arizona

Consumer financial obligation patterns in 2026 show a distinct shift in how homes manage their monthly responsibilities. With charge card APRs reaching historic highs for many locals in the United States, the need for proactive settlement has never ever been more evident. High interest rates do more than simply increase regular monthly payments. They extend the time it takes to clear a balance, typically turning a fairly little purchase into a multi-year monetary burden. Families in any given region are increasingly searching for ways to minimize the total expense of their borrowing to secure their long-lasting monetary health.

Direct settlement with lenders stays among the fastest ways to see a decrease in interest rates. In 2026, banks are often willing to listen to customers who have a history of on-time payments however are facing genuine financial pressure. A basic call to the customer support department can sometimes result in a temporary or irreversible rate decrease. Success in these conversations generally needs preparation. Understanding the present average rates and having a clear record of your commitment to the organization offers a strong foundation for the demand. Many individuals find that discussing a competing offer or talking about a short-lived difficulty can move the needle.

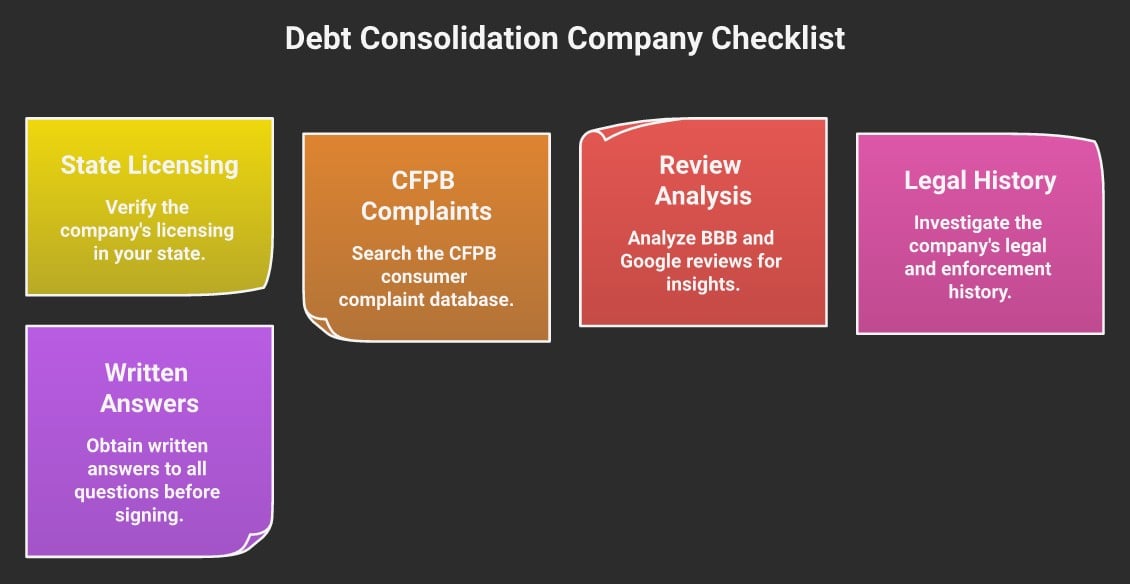

Professional assistance typically starts with understanding Debt Consolidation as a way to regain control. For those who find direct negotiation intimidating or unsuccessful, credit therapy firms provide a structured alternative. These organizations serve as intermediaries in between the consumer and the lender, utilizing established relationships to secure terms that an individual might not have the ability to get on their own. This is particularly effective for those carrying balances across multiple accounts, where handling several different interest rates becomes a logistical battle.

The Function of Nonprofit Credit Therapy in 2026

Not-for-profit credit counseling firms have actually seen a surge in demand throughout 2026 as more individuals look for options to high-interest financial obligation cycles. These agencies, typically 501(c)(3) companies, are required to act in the very best interest of the customer. Agencies with U.S. Department of Justice approval for pre-bankruptcy counseling offer a level of oversight that guarantees high requirements of service. These organizations offer more than simply rate negotiation. They supply extensive financial evaluations that look at earnings, expenses, and total financial obligation to develop a sustainable course forward.

Stats from early 2026 show that Integrated Debt Consolidation Programs has actually helped countless people prevent the long-lasting consequences of default. Among the main tools used by these firms is the debt management program. This program is not a loan but a repayment strategy where the firm works out with financial institutions to lower rates of interest and waive certain fees. Once the lenders accept the terms, the customer makes a single month-to-month payment to the company, which then disperses the funds to the various creditors. This combination simplifies the procedure and, more importantly, ensures that a bigger part of each payment goes toward the principal balance instead of interest charges.

Real estate counseling is another aspect of these not-for-profit services, especially for those in Surprise Arizona who are dealing with both customer debt and mortgage payments. Agencies authorized by the Department of Real Estate and Urban Development (HUD) can provide customized guidance that incorporates real estate stability with financial obligation decrease. This holistic approach is vital in the 2026 economy, where housing costs and charge card interest are frequently the 2 largest elements of a home budget.

Working Out with Modern Creditors in the Current Market

The financial environment of 2026 has actually altered how lenders view danger. Algorithms now play a bigger role in determining who gets a rate decrease. Preserving a constant payment history is still the most significant factor, but creditors also look at total debt-to-income ratios. For citizens of the local community, knowing these internal bank metrics can assist throughout a negotiation. If a bank sees that a client is proactively looking for financial literacy education, they might see that client as a lower threat, making them more open to reducing rates.

Financial literacy programs have actually broadened significantly this year. Numerous nonprofit agencies now partner with regional financial institutions and neighborhood groups to supply complimentary workshops and online tools. These programs cover everything from standard budgeting to sophisticated debt repayment strategies. By getting involved in these academic tracks, customers acquire the vocabulary and the self-confidence needed to speak with their banks. Understanding the difference between a standard APR and a penalty APR is a standard however powerful piece of understanding in any negotiation.

Organizations increasingly rely on Debt Consolidation in Surprise to stay competitive, and consumers should embrace a comparable state of mind toward their personal financial resources. Treating financial obligation management as a strategic task rather than a source of tension causes better outcomes. For instance, understanding that some financial institutions use "hardship programs" that are separate from their standard client service scripts can change the whole instructions of a negotiation. These programs are specifically created for individuals experiencing momentary obstacles, such as a medical emergency or a task modification, and they typically consist of significant rates of interest caps for a set period.

Combining for Lower Rates in Surprise Arizona

Debt debt consolidation is frequently confused with getting a new loan to settle old ones. While that is one technique, the debt management programs offered by not-for-profit companies in 2026 provide a different path. These programs do not require a high credit history for entry, which makes them accessible to people who have actually currently seen their scores dip due to high balances. By combining payments into one lower monthly amount, the emotional problem of debt is reduced along with the financial expense. The reduced rates of interest worked out by the agency are frequently locked in throughout of the program, supplying a predictable timeline for ending up being debt-free.

:max_bytes(150000):strip_icc()/best-personal-loans-for-debt-consolidation-4779764-FINAL-1-3-27966a22e0ea417ab5a0f1274c10f529.png)

Agencies running nationwide, including those with geo-specific services across all 50 states, have actually established networks of independent affiliates. This makes sure that an individual in Surprise Arizona can get recommendations that thinks about regional financial conditions while gaining from the scale and working out power of a bigger organization. These collaborations enable a more customized touch, where counselors understand the specific obstacles of the regional job market or expense of living.

Pre-discharge debtor education and pre-bankruptcy counseling are also critical services supplied by these companies. While the goal is typically to prevent bankruptcy, these sessions are needed by law for those who do proceed with a filing. In 2026, these academic requirements are viewed as a method to guarantee that individuals have the tools to rebuild their credit and avoid falling back into high-interest financial obligation traps in the future. Even for those ruling out bankruptcy, the lessons taught in these sessions-- such as tracking every dollar and comprehending the real cost of credit-- are widely relevant.

Long-Term Financial Stability Beyond 2026

Minimizing interest rates is a vital step, however preserving that progress needs a shift in how credit is utilized. The goal of any settlement or financial obligation management strategy is to develop adequate room in the budget to begin building an emergency fund. Without a cash cushion, many individuals discover themselves grabbing high-interest charge card the moment an unforeseen cost arises. Counselors in 2026 stress that the genuine triumph isn't simply a lower APR, but the ability to stop counting on credit for everyday living expenditures.

The rise of co-branded partner programs has actually made it easier for people to gain access to aid through their workplaces or local neighborhood. These programs typically integrate debt management with broader wellness initiatives, acknowledging that monetary tension has a direct effect on physical and mental health. By bringing these services into the neighborhood, companies are reaching people previously in the financial obligation cycle, before the circumstance becomes a crisis.

Financial self-reliance in any state during 2026 is achieved through a combination of aggressive rate negotiation, expert support, and disciplined budgeting. Whether through a direct call to a bank or a structured strategy with a not-for-profit firm, the resources offered today are more accessible than ever. Taking the first step to deal with high rates of interest can conserve countless dollars and years of stress, permitting families to concentrate on their future rather than their previous financial obligations.

{kind=link}

Latest Posts

Decreasing Interest Costs for Surprise Arizona

The Impact of 2026 Rate Of Interest on Personal Budget Plans

Improving Month-to-month Money Flow With Regional Combination Experts